What is the Ultra-Thin Glass Market Overview – definition, scope, and significance?

Ultra-thin glass (UTG) refers to glass sheets whose thickness ranges from 30 µm to 200 µm, produced through specialized float and fusion processes that enable exceptional flexibility, optical clarity, and strength. The market encompasses the design, manufacturing, and supply of UTG for a variety of end‑use applications such as semiconductor substrates, flat‑panel displays, touch‑control devices, automotive glazing, and medical devices. Its significance stems from the material’s ability to replace traditional substrates like plastic and thick glass, offering superior durability, heat resistance, and recyclability while supporting the miniaturization and weight‑reduction trends in modern electronics, automotive, and healthcare products.

What are the Ultra-Thin Glass Market drivers, restraints, challenges, and opportunities?

Key drivers include the relentless demand for slimmer, lighter consumer electronics, the expansion of foldable and flexible display technologies, and the automotive industry's shift toward lightweight glazing for improved fuel efficiency. Growth is further bolstered by increasing adoption of UTG in semiconductor wafers, where its superior flatness enhances yield. Restraints involve high capital expenditure for specialized float‑fusion lines and the relatively higher cost of UTG compared with polymer alternatives. Major challenges are related to scaling production while maintaining defect‑free quality, and navigating stringent safety standards for automotive glazing. Opportunities arise from emerging medical‑device applications that require biocompatible, thin, and robust glass, as well as from potential partnerships with display manufacturers developing next‑generation flexible screens.

What are the Ultra-Thin Glass Market growth trends?

The market is trending toward integration of UTG in foldable smartphones and rollable televisions, which demand thicknesses below 100 µm without compromising rigidity. Another notable trend is the use of UTG as a barrier layer in flexible printed circuit boards, improving electromagnetic shielding. In the automotive sector, manufacturers are experimenting with UTG for head‑up display (HUD) panels and panoramic roofs that combine transparency with impact resistance. Regionally, Asia‑Pacific remains the primary hub for production due to the concentration of glass manufacturers, while North America shows rapid adoption in high‑end medical imaging equipment.

How has COVID‑19 impacted the Ultra-Thin Glass Market and what is the recovery trajectory?

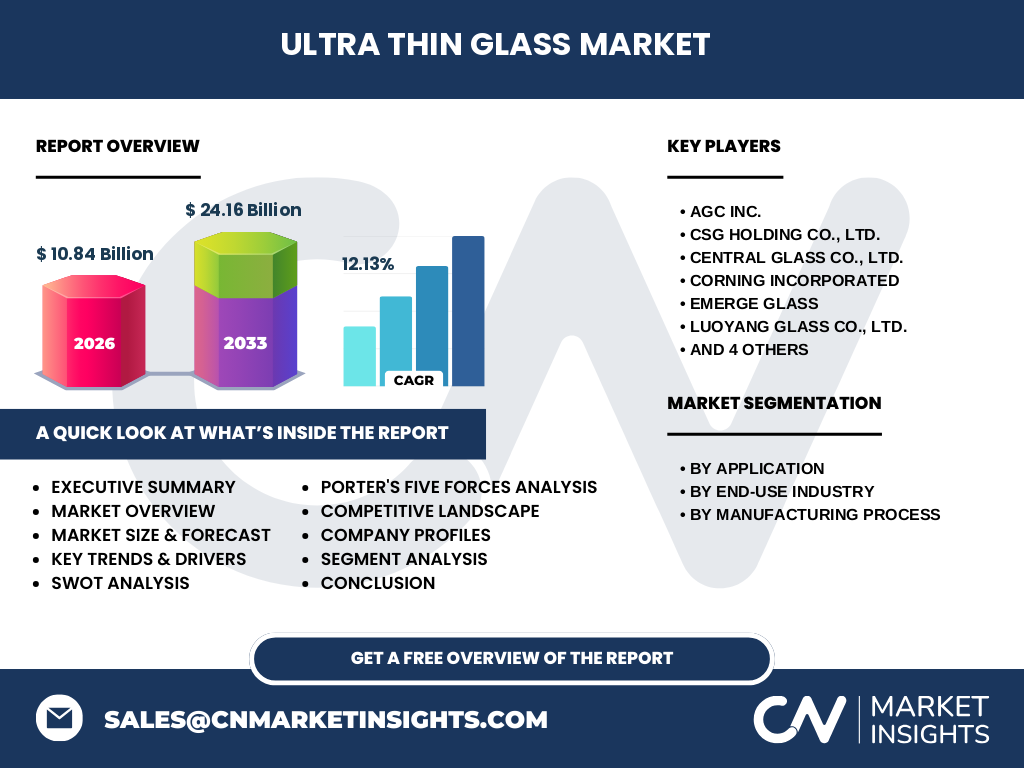

The pandemic caused temporary disruptions in supply chains, particularly affecting raw‑material logistics and equipment installation for new float‑fusion lines. Demand from consumer electronics contracted in 2020 as production shifted to remote work, but rebounded strongly in 2021‑2022 with the surge in smartphones and remote‑learning devices. Automotive demand slowed during lockdowns but recovered as manufacturers resumed production and introduced lightweight glazing solutions. Overall, the market demonstrated resilience, and the current trajectory points to a robust post‑COVID expansion, reflected in a projected CAGR of 12.13 % through 2033.

What does the Ultra-Thin Glass Market competitive landscape look like?

The competitive landscape is characterized by a few large, vertically integrated glass producers and several specialized niche players. Major competitors such as Corning Incorporated, SCHOTT AG, and AGC Inc. dominate the high‑technology segment with extensive R&D capabilities. Asian manufacturers including CSG Holding Co., Ltd., Central Glass Co., Ltd., and Xinyi Glass Holdings Limited leverage cost‑effective production to capture volume market share. Recent years have seen consolidation through strategic acquisitions and joint ventures aimed at expanding float‑fusion capacities and securing long‑term supply contracts with display and automotive OEMs.

What are the key findings in the Executive Summary?

The Ultra‑Thin Glass market is poised for rapid expansion, reaching a projected value of $24.16 billion by 2033 from $10.84 billion in 2026, driven by a 12.13 % CAGR. Growth is underpinned by strong demand from flexible display manufacturers, automotive glazing innovations, and semiconductor substrate applications. While high capital costs and production complexity pose barriers, ongoing investments in advanced float‑fusion technology and strategic partnerships are mitigating these risks. The market is increasingly competitive, with both legacy glass giants and agile Asian firms vying for leadership across application segments.

What are the Ultra-Thin Glass Market forecasts for 2025‑2032?

Based on the provided CAGR of 12.13 %, the market is expected to maintain steady double‑digit growth throughout the forecast horizon. By the end of 2032, the market size is anticipated to approach the $24 billion mark, reflecting sustained adoption across consumer‑electronics, automotive, and medical sectors. The forecast assumes continued investment in flexible display lines, expansion of UTG‑based automotive glazing, and incremental penetration in semiconductor substrate applications.

How is the Ultra-Thin Glass Market sized and shared by segmentation?

Segmentation by application shows three primary pillars: Semiconductor Substrate, Flat Panel Displays & Touch Control Devices, and Automotive Glazing. By end‑use industry, the market splits among Consumer Electronics, Automotive, and Medical & Healthcare. Manufacturing processes are categorized into Float and Fusion techniques, which together supply all application segments. While exact share percentages are not disclosed, the dominance of consumer‑electronics and display applications is evident from industry trends, with automotive glazing emerging as a fast‑growing niche, and semiconductor substrates contributing a stable, high‑value portion.

What is the global Ultra-Thin Glass Market size and share by region?

The global market is anchored by major production hubs in Asia‑Pacific, which hosts the majority of float‑fusion facilities and supplies both domestic and export demand. North America and Europe hold significant shares due to high consumption in advanced electronics, automotive, and medical devices. Although precise regional monetary values are not provided, the overall market size of $10.84 billion in 2026 reflects the combined contribution of these regions, with Asia‑Pacific contributing the largest proportion.

What does the regional analysis of the Ultra-Thin Glass Market reveal?

Asia‑Pacific leads in capacity expansion, driven by China, Japan, and South Korea’s investments in flexible display factories and automotive glazing projects. North America’s growth is propelled by premium consumer‑electronics and medical‑device manufacturers demanding high‑precision UTG. Europe shows steady demand in automotive safety glazing and aerospace applications. Emerging markets in Latin America and the Middle East are beginning to adopt UTG for niche automotive and consumer‑electronics projects, indicating potential future growth.

What are the leading company profiles in the Ultra-Thin Glass Market?

Corning Incorporated leverages its Gorilla® Glass heritage to develop ultra‑thin variants for foldable phones. SCHOTT AG focuses on high‑purity glass for semiconductor substrates. AGC Inc. combines its float‑glass expertise with UTG R&D to serve automotive glazing. Asian leaders such as CSG Holding Co., Ltd., Central Glass Co., Ltd., and Xinyi Glass Holdings Limited emphasize cost‑efficient production and supply chain integration. Nippon Electric Glass Co., Ltd. and Nippon Sheet Glass Co., Ltd. specialize in precision float‑fusion processes for display panels. Luoyang Glass Co., Ltd. and Emerge Glass target emerging applications in medical devices.

How does Porter’s Five Forces analysis apply to the Ultra-Thin Glass Market?

Threat of new entrants is moderate; high capital requirements and specialized technology create barriers, but Asian manufacturers can enter via joint ventures. Bargaining power of suppliers is relatively low because raw silica and chemicals are widely available, though specialty chemicals for fusion processes can be scarce. Bargaining power of buyers is high, especially large OEMs that demand volume discounts and custom specifications. Threat of substitutes is moderate; polymer substrates offer lower cost but lack UTG’s durability and heat resistance. Industry rivalry is intense, with legacy glass firms and agile Asian players competing on technology, price, and capacity.

What is the SWOT analysis of the Ultra-Thin Glass Market?

Strengths: Superior mechanical strength, optical clarity, and recyclability; suitability for flexible and lightweight designs. Weaknesses: Higher production cost and complexity; limited supplier base for high‑precision float‑fusion equipment. Opportunities: Expansion into foldable displays, automotive HUDs, and medical imaging; strategic alliances with semiconductor fabs. Threats: Rapid technological shifts toward alternative substrates; potential supply‑chain disruptions for specialty chemicals.

What does the Ultra-Thin Glass market value chain look like?

The value chain begins with raw material procurement (silica sand, soda ash, specialty chemicals), proceeds to float or fusion melting, followed by precision thinning, annealing, and coating processes. Subsequent stages include quality inspection, cutting to customer‑specified dimensions, and logistics to OEMs in electronics, automotive, and medical sectors. Ancillary services such as R&D collaboration, custom formulation, and after‑sales technical support add value throughout the chain.

What are the key investment insights for the Ultra-Thin Glass Market?

Investors should focus on companies with proven float‑fusion capabilities and strong R&D pipelines for flexible display applications. Partnerships with major smartphone and automotive OEMs provide predictable revenue streams. Allocating capital to expand capacity in Asia‑Pacific can capture the fastest‑growing demand. Monitoring emerging medical‑device entrants offers a secondary growth avenue, while diversifying across both consumer‑electronics and automotive segments reduces exposure to sector‑specific cycles.

What conclusions can be drawn from the Ultra-Thin Glass Market analysis?

The Ultra‑Thin Glass market is on a high‑growth trajectory, underpinned by structural shifts toward lighter, thinner, and more durable components across key industries. Despite cost and technical barriers, ongoing innovation and strategic collaborations are driving adoption. The market’s projected value of $24.16 billion by 2033 underscores its relevance, and the competitive environment suggests that firms able to deliver high‑quality, low‑defect products at scale will command the greatest market share.

What research methodology was used for this Ultra-Thin Glass Market report?

The study combined primary interviews with industry experts, supplier surveys, and secondary data extraction from company annual reports, press releases, and reputable market databases. Quantitative forecasting employed CAGR calculations based on the provided 2026 market size ($10.84 billion) and the 2027‑2033 projection ($24.16 billion). Qualitative insights were derived from trend analysis, technology roadmaps, and competitive positioning.

What is the scope of the Ultra-Thin Glass Market research?

The research covers global market dynamics, segmentation by application, end‑use industry, and manufacturing process, as well as regional performance for major geographic zones. It includes competitive profiling of the ten listed key companies, value‑chain assessment, and strategic analyses (Porter, SWOT). The scope does not extend to detailed pricing benchmarks or proprietary cost structures, focusing instead on market size, growth drivers, and strategic outlook.

Which key companies and recent developments define the Ultra-Thin Glass Market?

Corning Incorporated announced a new ultra‑thin glass line optimized for foldable smartphones, partnering with leading handset manufacturers. SCHOTT AG launched a high‑purity UTG substrate for next‑generation semiconductor wafers. AGC Inc. unveiled a lightweight automotive glazing solution targeting electric‑vehicle manufacturers. CSG Holding Co., Ltd. reported a capacity expansion in its float‑fusion plant to meet rising display demand. Xinyi Glass Holdings Limited entered a joint venture with a European automotive supplier to develop HUD glass. Nippon Electric Glass Co., Ltd. introduced a proprietary coating that enhances UTG scratch resistance, expanding its appeal in premium consumer devices.